|

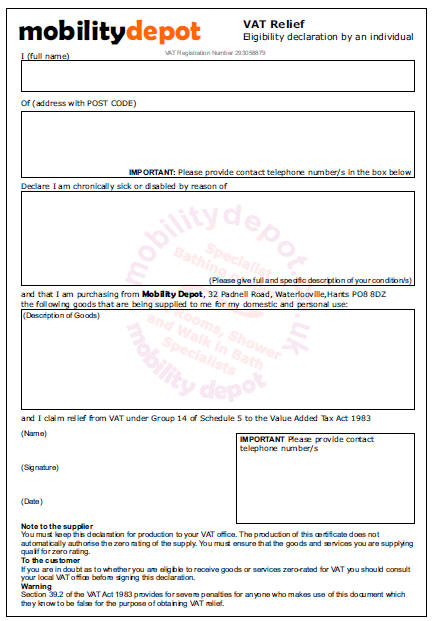

If you believe you

qualify for relief from paying VAT when making a purchase (for any

reason) you must provide a signed declaration to support your claim

prior to us processing your order.

You will need to complete an

'Eligibility

Declaration Form'

. This will accompany your order and be made available to HM Revenue &

Customs for inspection should they so wish. This simple statement sets out what you are

purchasing and the reason you are claiming relief. Your details will

remain confidential.

Submitting this form does not automatically make you eligible.

If you are unsure whether you may be entitled to relief please don't

hesitate to ask. It is better to ask rather than risk a false claim.

If for any reason we are unable to process your order excluding

VAT you will be notified. In this event, you will still be able to apply to HM

Customs and Excise for a refund.

|